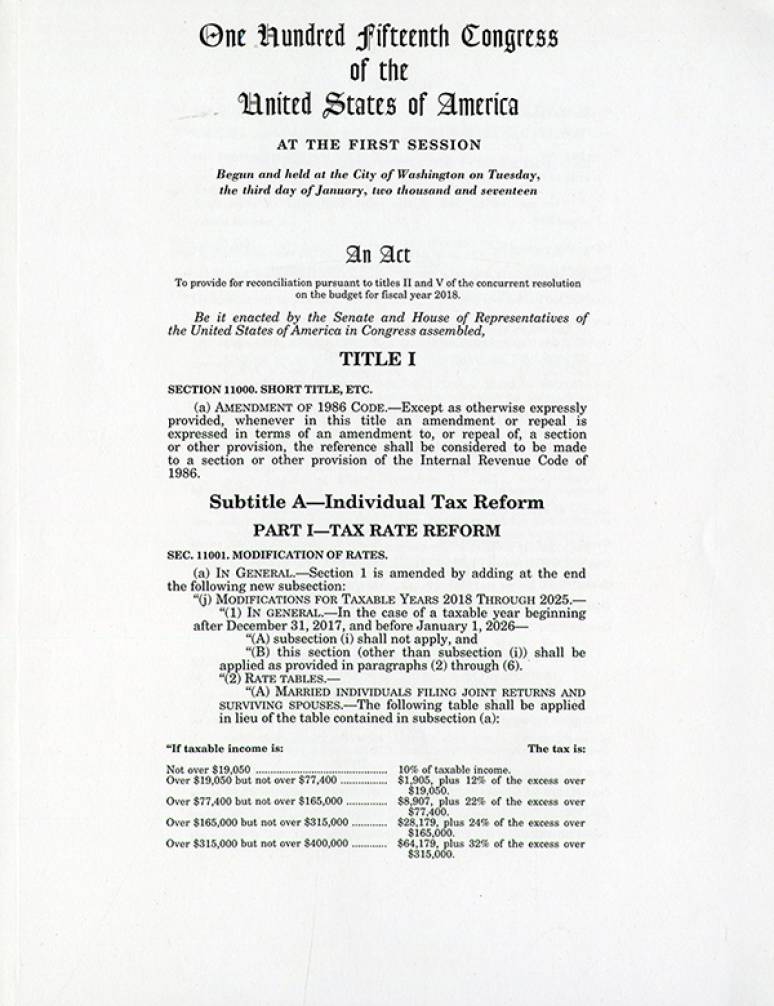

AN ACT To provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018. 1 Be it enacted by the Senate and House of Representatives of the United States of America in Congress assembled, 3 SECTION 1. SHORT TITLE; ETC. 4 (a) SHORT TITLE.—This Act may be cited as the 5 ‘‘Tax Cuts and Jobs Act’’. 6 (b) AMENDMENT OF 1986 CODE.—Except as otherwise expressly provided, whenever in this Act an amendment or repeal is expressed in terms of an amendment 9 to, or repeal of, a section or other provision, the reference VerDate Sep 11 2014 22:51 Nov 28, 2017 Jkt 079200 PO 00000 Frm 00001 Fmt 6652 Sfmt 6201 E:\BILLS\H1.PCS H1 daltland on DSK30NT082PROD with BILLS 2 HR 1 PCS 1 shall be considered to be made to a section or other provision of the Internal Revenue Code of 1986.

Sec. 1. Short title; etc. TITLE I—TAX REFORM FOR INDIVIDUALS Subtitle A—Simplification and Reform of Rates, Standard Deduction, and Exemptions Sec. 1001. Reduction and simplification of individual income tax rates. Sec. 1002. Enhancement of standard deduction. Sec. 1003. Repeal of deduction for personal exemptions. Sec. 1004. Maximum rate on business income of individuals. Sec. 1005. Conforming amendments related to simplification of individual income tax rates. Subtitle B—Simplification and Reform of Family and Individual Tax Credits Sec. 1101. Enhancement of child tax credit and new family tax credit. Sec. 1102. Repeal of nonrefundable credits. Sec. 1103. Refundable credit program integrity. Sec. 1104. Procedures to reduce improper claims of earned income credit. Sec. 1105. Certain income disallowed for purposes of the earned income tax credit. Subtitle C—Simplification and Reform of Education Incentives Sec. 1201. American opportunity tax credit. Sec. 1202. Consolidation of education savings rules. Sec. 1203. Reforms to discharge of certain student loan indebtedness. Sec. 1204. Repeal of other provisions relating to education. Sec. 1205. Rollovers between qualified tuition programs and qualified ABLE programs. Subtitle D—Simplification and Reform of Deductions Sec. 1301. Repeal of overall limitation on itemized deductions. Sec. 1302. Mortgage interest. Sec. 1303. Repeal of deduction for certain taxes not paid or accrued in a trade or business. Sec. 1304. Repeal of deduction for personal casualty losses. Sec. 1305. Limitation on wagering losses. Sec. 1306. Charitable contributions. Sec. 1307. Repeal of deduction for tax preparation expenses. Sec. 1308. Repeal of medical expense deduction. Sec. 1309. Repeal of deduction for alimony payments. Sec. 1310. Repeal of deduction for moving expenses. Sec. 1311. Termination of deduction and exclusions for contributions to medical savings accounts. VerDate Sep 11 2014 22:51 Nov 28, 2017 Jkt 079200 PO 00000 Frm 00002 Fmt 6652 Sfmt 6211 E:\BILLS\H1.PCS H1 daltland on DSK30NT082PROD with BILLS 3 HR 1 PCS Sec. 1312. Denial of deduction for expenses attributable to the trade or business of being an employee. Subtitle E—Simplification and Reform of Exclusions and Taxable Compensation Sec. 1401. Limitation on exclusion for employer-provided housing. Sec. 1402. Exclusion of gain from sale of a principal residence. Sec. 1403. Repeal of exclusion, etc., for employee achievement awards. Sec. 1404. Sunset of exclusion for dependent care assistance programs. Sec. 1405. Repeal of exclusion for qualified moving expense reimbursement. Sec. 1406. Repeal of exclusion for adoption assistance programs. Subtitle F—Simplification and Reform of Savings, Pensions, Retirement Sec. 1501. Repeal of special rule permitting recharacterization of Roth IRA contributions as traditional IRA contributions. Sec. 1502. Reduction in minimum age for allowable in-service distributions. Sec. 1503. Modification of rules governing hardship distributions. Sec. 1504. Modification of rules relating to hardship withdrawals from cash or deferred arrangements. Sec. 1505. Extended rollover period for the rollover of plan loan offset amounts in certain cases. Sec. 1506. Modification of nondiscrimination rules to protect older, longer service participants. Subtitle G—Estate, Gift, and Generation-skipping Transfer Taxes Sec. 1601. Increase in credit against estate, gift, and generation-skipping transfer tax. Sec. 1602. Repeal of estate and generation-skipping transfer taxes. TITLE II—ALTERNATIVE MINIMUM TAX REPEAL Sec. 2001. Repeal of alternative minimum tax. TITLE III—BUSINESS TAX REFORM Subtitle A—Tax Rates Sec. 3001. Reduction in corporate tax rate. Subtitle B—Cost Recovery Sec. 3101. Increased expensing. Subtitle C—Small Business Reforms Sec. 3201. Expansion of section 179 expensing. Sec. 3202. Small business accounting method reform and simplification. Sec. 3203. Small business exception from limitation on deduction of business interest. Sec. 3204. Modification of treatment of S corporation conversions to C corporations. Subtitle D—Reform of Business-related Exclusions, Deductions, etc. Sec. 3301. Interest. Sec. 3302. Modification of net operating loss deduction. VerDate Sep 11 2014 22:51 Nov 28, 2017 Jkt 079200 PO 00000 Frm 00003 Fmt 6652 Sfmt 6211 E:\BILLS\H1.PCS H1 daltland on DSK30NT082PROD with BILLS 4 HR 1 PCS Sec. 3303. Like-kind exchanges of real property. Sec. 3304. Revision of treatment of contributions to capital. Sec. 3305. Repeal of deduction for local lobbying expenses. Sec. 3306. Repeal of deduction for income attributable to domestic production activities. Sec. 3307. Entertainment, etc. expenses. Sec. 3308. Unrelated business taxable income increased by amount of certain fringe benefit expenses for which deduction is disallowed. Sec. 3309. Limitation on deduction for FDIC premiums. Sec. 3310. Repeal of rollover of publicly traded securities gain into specialized small business investment companies. Sec. 3311. Certain self-created property not treated as a capital asset. Sec. 3312. Repeal of special rule for sale or exchange of patents. Sec. 3313. Repeal of technical termination of partnerships. Sec. 3314. Recharacterization of certain gains in the case of partnership profits interests held in connection with performance of investment services. Sec. 3315. Amortization of research and experimental expenditures. Sec. 3316. Uniform treatment of expenses in contingency fee cases. Subtitle E—Reform of Business Credits Sec. 3401. Repeal of credit for clinical testing expenses for certain drugs for rare diseases or conditions. Sec. 3402. Repeal of employer-provided child care credit. Sec. 3403. Repeal of rehabilitation credit. Sec. 3404. Repeal of work opportunity tax credit. Sec. 3405. Repeal of deduction for certain unused business credits. Sec. 3406. Termination of new markets tax credit. Sec. 3407. Repeal of credit for expenditures to provide access to disabled individuals. Sec. 3408. Modification of credit for portion of employer social security taxes paid with respect to employee tips. Subtitle F—Energy Credits Sec. 3501. Modifications to credit for electricity produced from certain renewable resources. Sec. 3502. Modification of the energy investment tax credit. Sec. 3503. Extension and phaseout of residential energy efficient property. Sec. 3504. Repeal of enhanced oil recovery credit. Sec. 3505. Repeal of credit for producing oil and gas from marginal wells. Sec. 3506. Modifications of credit for production from advanced nuclear power facilities. Subtitle G—Bond Reforms Sec. 3601. Termination of private activity bonds. Sec. 3602. Repeal of advance refunding bonds. Sec. 3603. Repeal of tax credit bonds. Sec. 3604. No tax exempt bonds for professional stadiums. Subtitle H—Insurance Sec. 3701. Net operating losses of life insurance companies. Sec. 3702. Repeal of small life insurance company deduction. Sec. 3703. Surtax on life insurance company taxable income. VerDate Sep 11 2014 22:51 Nov 28, 2017 Jkt 079200 PO 00000 Frm 00004 Fmt 6652 Sfmt 6211 E:\BILLS\H1.PCS H1 daltland on DSK30NT082PROD with BILLS 5 HR 1 PCS Sec. 3704. Adjustment for change in computing reserves. Sec. 3705. Repeal of special rule for distributions to shareholders from pre- 1984 policyholders surplus account. Sec. 3706. Modification of proration rules for property and casualty insurance companies. Sec. 3707. Modification of discounting rules for property and casualty insurance companies. Sec. 3708. Repeal of special estimated tax payments. Subtitle I—Compensation Sec. 3801. Modification of limitation on excessive employee remuneration. Sec. 3802. Excise tax on excess tax-exempt organization executive compensation. Sec. 3803. Treatment of qualified equity grants. TITLE IV—TAXATION OF FOREIGN INCOME AND FOREIGN PERSONS

Subtitle A—Establishment of Participation Exemption System for Taxation of Foreign Income Sec. 4001. Deduction for foreign-source portion of dividends received by domestic corporations from specified 10-percent owned foreign corporations. Sec. 4002. Application of participation exemption to investments in United States property. Sec. 4003. Limitation on losses with respect to specified 10-percent owned foreign corporations. Sec. 4004. Treatment of deferred foreign income upon transition to participation exemption system of taxation.

Subtitle B—Modifications Related to Foreign Tax Credit System Sec. 4101. Repeal of section 902 indirect foreign tax credits; determination of section 960 credit on current year basis. Sec. 4102. Source of income from sales of inventory determined solely on basis of production activities.

Subtitle C—Modification of Subpart F Provisions Sec. 4201. Repeal of inclusion based on withdrawal of previously excluded subpart F income from qualified investment. Sec. 4202. Repeal of treatment of foreign base company oil related income as subpart F income. Sec. 4203. Inflation adjustment of de minimis exception for foreign base company income. Sec. 4204. Look-thru rule for related controlled foreign corporations made permanent. Sec. 4205. Modification of stock attribution rules for determining status as a controlled foreign corporation. Sec. 4206. Elimination of requirement that corporation must be controlled for 30 days before subpart F inclusions apply.

Subtitle D—Prevention of Base Erosion Sec. 4301. Current year inclusion by United States shareholders with foreign high returns. VerDate Sep 11 2014 22:51 Nov 28, 2017 Jkt 079200 PO 00000 Frm 00005 Fmt 6652 Sfmt 6211 E:\BILLS\H1.PCS H1 daltland on DSK30NT082PROD with BILLS 6 HR 1 PCS Sec. 4302. Limitation on deduction of interest by domestic corporations which are members of an international financial reporting group. Sec. 4303. Excise tax on certain payments from domestic corporations to related foreign corporations; election to treat such payments as effectively connected income.

Subtitle E—Provisions Related to Possessions of the United States Sec. 4401. Extension of deduction allowable with respect to income attributable to domestic production activities in Puerto Rico. Sec. 4402. Extension of temporary increase in limit on cover over of rum excise taxes to Puerto Rico and the Virgin Islands. Sec. 4403. Extension of American Samoa economic development credit.

Subtitle F—Other International Reforms Sec. 4501. Restriction on insurance business exception to passive foreign investment company rules.

TITLE V—EXEMPT ORGANIZATIONS

Subtitle A—Unrelated Business Income Tax Sec. 5001. Clarification of unrelated business income tax treatment of entities treated as exempt from taxation under section 501(a). Sec. 5002. Exclusion of research income limited to publicly available research.

Subtitle B—Excise Taxes Sec. 5101. Simplification of excise tax on private foundation investment income. Sec. 5102. Private operating foundation requirements relating to operation of art museum. Sec. 5103. Excise tax based on investment income of private colleges and universities. Sec. 5104. Exception from private foundation excess business holding tax for independently-operated philanthropic business holdings.

Subtitle C—Requirements for Organizations Exempt From Tax Sec. 5201. 501(c)(3) organizations permitted to make statements relating to political campaign in ordinary course of activities. Sec. 5202. Additional reporting requirements for donor advised fund sponsoring organizations.

Sec. 5201. 501(c)(3) organizations permitted to make statements relating to political campaign in ordinary course of activities.

Sec. 5202. Additional reporting requirements for donor advised fund sponsoring organizations.

Members of Congress, U.S. taxpayers, Amendment of 1986 Tax Code, accountants, cpas, tax preparers, educators and students of the U.S tax code

Product Details

- H.R. 1, Individual Tax Reform

- Tax Reform

- Taxation